Buy-to-Let Mortgage with No Proof of Income

Property investors often ask whether it is possible to secure a buy-to-let mortgage without traditional…

What Is the Minimum Rental Income Required for a…

If you are applying for a buy-to-let mortgage in the UK, one of the most…

Buy-to-Let Mortgage for Leasehold Properties: What Landlords Need to…

Buying a leasehold property as a landlord can be profitable, but it also introduces additional…

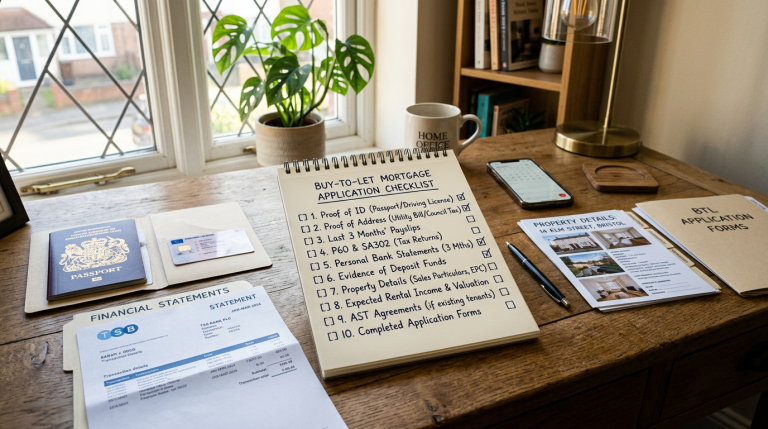

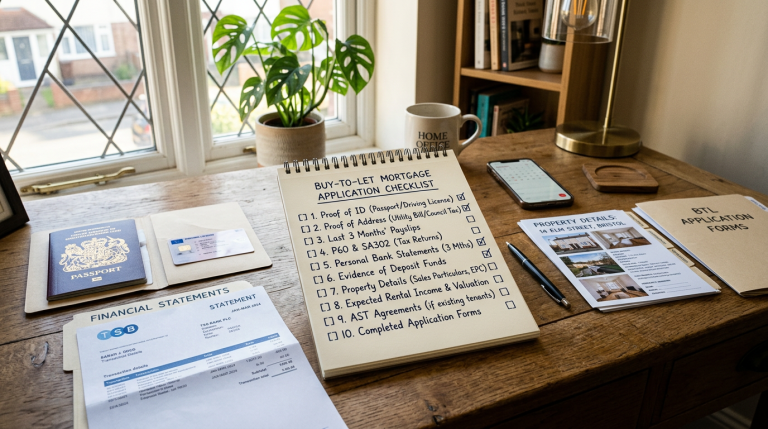

Buy-to-Let Mortgage Application Documents: Complete Checklist

Applying for a buy-to-let mortgage can feel straightforward until the lender asks for documents. Many…

How Many Buy-to-Let Mortgages Can You Have at Once?

Building a property portfolio is one of the most common ways UK landlords generate long-term…

HMO Buy-to-Let Mortgage for Houses in Multiple Occupation

An HMO buy-to-let mortgage is a specialist finance product for landlords buying or refinancing a…

Living in BTL Property: Can You Live in a…

Living in BTL property may sound harmless if you own the property, the tenant has…

Student Let BTL Mortgage: Buy-to-Let Finance for Student Accommodation

Student accommodation can be one of the most attractive areas of the UK rental market,…

How Rental Yield Affects Your Buy-to-Let Mortgage Application

A strong rental yield can make a buy-to-let investment look attractive, but lenders do not…