Buying a leasehold property as a landlord can be profitable, but it also introduces additional rules, lender requirements, and long-term risks that many investors overlook. Whether you are buying a city-centre apartment, an ex-council flat, or a modern development, understanding how a leasehold BTL mortgage works is essential before committing to a purchase.

Unlike freehold properties, leasehold homes come with a diminishing lease term, service charges, ground rent obligations, and restrictions imposed by the freeholder or managing agent. These factors directly affect mortgage approval, rental profitability, resale value, and future refinancing opportunities.

This guide explains everything landlords need to know about leasehold buy-to-let mortgages in the UK, including lender criteria, short lease issues, costs, risks, and strategies for maximising rental returns.

What Is a Leasehold Buy-to-Let Mortgage?

A leasehold BTL mortgage is a mortgage designed for landlords purchasing a leasehold property to rent out to tenants.

With leasehold ownership, you own the property for a fixed number of years under a lease agreement, but not the land it stands on. Ownership eventually reverts to the freeholder once the lease expires unless it is extended.

Common leasehold properties include:

- Flats and apartments

- Maisonettes

- Some new-build houses

- Ex-council properties

- Retirement apartments

Most lenders provide buy-to-let finance for leasehold properties, but they usually apply stricter criteria than for freehold homes.

Why Leasehold Properties Are Popular With Landlords

Despite additional complexity, leasehold properties remain attractive investments for many landlords.

Lower Purchase Prices

Leasehold flats are often cheaper than freehold houses in the same location, reducing entry costs for investors.

Strong Rental Demand

Apartments in major UK cities frequently attract:

- Young professionals

- Students

- Corporate tenants

- International renters

Better Urban Locations

Leasehold properties are commonly located near:

- Transport hubs

- Universities

- Business districts

- Regeneration zones

Lower Maintenance Responsibility

External maintenance is often handled by the management company, which can reduce landlord workload.

How Lenders Assess a Leasehold BTL Mortgage

Mortgage lenders assess leasehold properties differently from freehold properties because lease terms and ongoing costs affect security value.

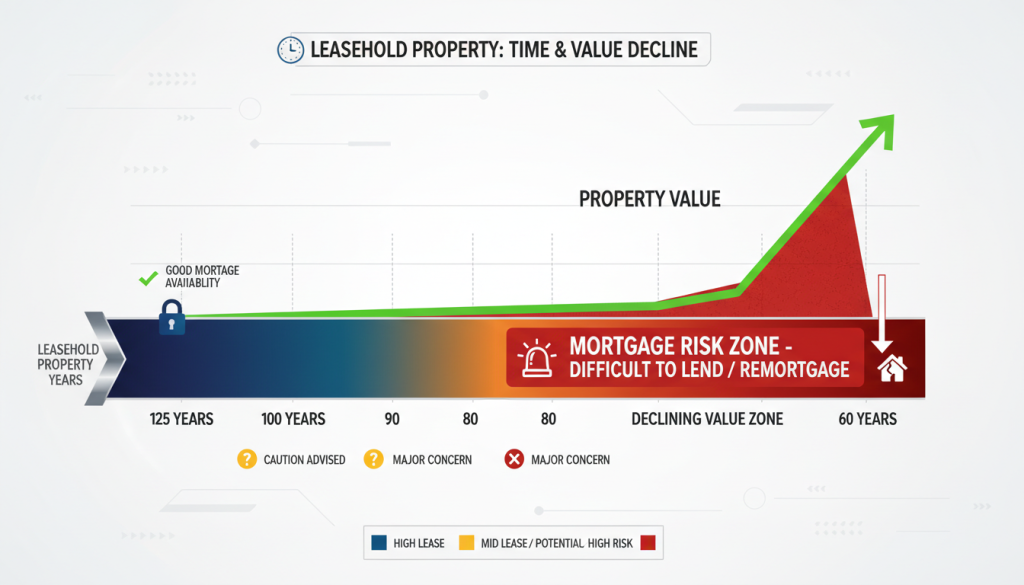

Remaining Lease Length

This is one of the most important factors.

Most lenders require:

- At least 70–85 years remaining at mortgage completion

- Some specialist lenders accept shorter leases

- Many require 30 years remaining after mortgage term ends

Properties with short leases are viewed as higher risk because value declines as the lease reduces.

Ground Rent

Lenders now scrutinise escalating ground rent clauses carefully.

Problematic leases may include:

- Ground rent doubling every 10 years

- High annual increases

- Onerous review periods

Some lenders decline properties entirely if the ground rent structure is considered unfair.

Service Charges

Service charges reduce rental profitability and affect affordability calculations.

Lenders consider:

- Annual maintenance fees

- Reserve fund contributions

- Building insurance costs

- Upcoming major works

Rental Coverage

Most lenders require projected rent to cover mortgage payments by 125%–145%.

For example:

- Monthly mortgage interest: £1,000

- Required rental coverage at 145%: £1,450+

Property Type

Certain leasehold properties can be harder to finance, including:

- Ex-local authority flats

- High-rise buildings

- Studio apartments

- Properties above commercial units

What Is Considered a Short Lease for BTL Mortgages?

A short lease typically means fewer than 80 years remaining.

Once a lease falls below 80 years:

- Mortgage options reduce significantly

- Property value declines faster

- Lease extension costs rise sharply

- Resale becomes harder

This is because “marriage value” becomes payable during lease extension calculations after the 80-year threshold.

Can You Get a Buy-to-Let Mortgage on a Short Lease Property?

Yes, but options become more limited.

Some specialist lenders may consider:

- 60–70 years remaining

- Experienced landlords

- Higher deposits

- Strong rental yields

However, landlords should carefully assess long-term costs before purchasing.

Common Short Lease Challenges

| Issue | Impact |

| Fewer lenders | Reduced mortgage choice |

| Higher rates | Increased borrowing costs |

| Lower valuations | Reduced loan sizes |

| Difficult refinancing | Future remortgage issues |

| Lower resale appeal | Smaller buyer pool |

Lease Extension Costs: What Landlords Must Consider

Lease extensions can be expensive, especially in high-value areas.

Costs may include:

- Premium paid to freeholder

- Solicitor fees

- Valuation fees

- Land Registry charges

- Freeholder legal costs

In some London locations, extending a short lease can cost tens of thousands of pounds.

Landlords should factor this into their investment calculations before purchasing.

Typical Deposit Requirements for Leasehold Landlord Finance

Most leasehold BTL mortgages require deposits between:

- 20% to 25% for standard cases

- 30% to 40% for higher-risk properties

- Larger deposits for short lease flats

Factors affecting deposit size include:

- Property location

- Lease term

- Credit history

- Rental yield

- Property condition

Leasehold Flats vs Freehold Houses for Landlords

| Factor | Leasehold Flat | Freehold House |

| Purchase price | Usually lower | Usually higher |

| Service charges | Yes | No |

| Ground rent | Often applicable | Usually none |

| Maintenance | Shared responsibility | Landlord responsibility |

| Lease expiry risk | Yes | No |

| Urban demand | Strong | Varies |

| Mortgage complexity | Higher | Lower |

Both can perform well as investments depending on strategy and location.

Hidden Costs Many Landlords Overlook

Many first-time investors focus solely on mortgage payments and rental income.

However, leasehold properties often include additional costs that impact profitability.

Common Costs Include

- Service charges

- Ground rent

- Building insurance contributions

- Managing agent fees

- Section 20 major works

- Lease extension costsHow Service Charges Affect Rental Yield

- Licence to let fees

Unexpected building works can significantly reduce annual profits.

How Service Charges Affect Rental Yield

High service charges can reduce cash flow substantially.

For example:

| Annual Rent | £18,000 |

| Mortgage Costs | £10,500 |

| Service Charges | £3,000 |

| Ground Rent | £350 |

| Net Income Before Tax | £4,150 |

Modern developments with concierge services, gyms, or lifts often carry higher management fees.

Landlords should request a full service charge history before proceeding.

Buying an Ex-Council Leasehold Flat

Ex-council properties can offer strong rental yields and lower purchase prices.

However, lenders may apply restrictions based on:

- Number of storeys

- Construction type

- Local authority ownership percentage

- Cladding concerns

- Building condition

Some lenders refuse tower blocks entirely.

Cladding and EWS1 Requirements

Following UK building safety reforms, many lenders require an EWS1 form for flats in certain buildings.

Without acceptable fire safety documentation:

- Mortgage approval may be delayed

- Valuations may be reduced

- Sales can collapse

This remains a major consideration for apartment investors.

Leasehold Restrictions That Affect Landlords

Some leases include restrictions that limit rental flexibility.

These may include:

- No Airbnb or short lets

- Pet restrictions

- Subletting approval requirements

- Tenant type limitations

- Alteration restrictions

Always review the lease carefully with a solicitor before exchange.

Interest Rates for Leasehold BTL Mortgages

Leasehold properties do not automatically mean higher mortgage rates, but short leases or high-risk buildings can increase pricing.

Rates are influenced by:

- Deposit size

- Credit score

- Rental income

- Lease term

- Property type

- Landlord experience

Experienced landlords with strong yields often access the best products.

Limited Company Leasehold BTL Mortgages

Many landlords now purchase through limited companies for tax planning purposes.

Benefits may include:

- Corporation tax efficiencies

- Easier portfolio growth

- Mortgage interest treatment advantages

- Succession planning

However, company mortgage rates and fees may differ from personal buy-to-let products.

Common Mistakes Landlords Make With Leasehold Properties

Ignoring Lease Length

Many investors underestimate how quickly a lease depreciates.

Underestimating Service Charges

Service charges can increase dramatically over time.

Failing to Check Ground Rent Clauses

Onerous leases can affect future mortgageability.

Not Reviewing Major Works Notices

Large building repairs can create unexpected costs.

Buying Without Specialist Advice

Leasehold investing involves legal and financial complexity that requires expert guidance.

How to Improve Mortgage Approval Chances

Landlords can strengthen applications by:

- Choosing properties with 85+ years remaining

- Keeping strong credit profiles

- Providing larger deposits

- Demonstrating rental income potential

- Working with specialist BTL mortgage brokers

- Avoiding problematic lease clauses

Case Example: Leasehold Flat Investment Analysis

Scenario

- Purchase price: £240,000

- Deposit: 25%

- Mortgage: £180,000

- Annual rent: £19,200

- Service charge: £2,400

- Ground rent: £250

Outcome

Although the rental yield initially appeared attractive, net profitability reduced after management costs and leasehold expenses were included.

However, the property still performed well due to:

- Strong tenant demand

- Excellent transport links

- Long lease term

- High occupancy rates

This highlights why landlords must analyse total ownership costs rather than purchase price alone.

Why Many Investors Still Prefer Leasehold Flats

Despite added complexity, leasehold properties remain a core part of many landlord portfolios.

Key reasons include:

- Lower entry costs

- Strong city demand

- Consistent tenant pools

- Easier diversification

- Potential capital appreciation in regeneration areas

When properly researched, leasehold investments can generate strong long-term returns.

How Lockwell Finance Can Help

Finding the right leasehold BTL mortgage requires specialist knowledge of:

- Short lease lending

- Rental stress testing

- Limited company structures

- Ex-council lending

- Portfolio landlord finance

- Complex property scenarios

At Lockwell Finance, we help landlords secure tailored mortgage solutions for leasehold properties across the UK.

Whether you are buying your first rental flat or refinancing a large portfolio, our advisers can help you compare lender criteria and structure the right finance solution.

Why Landlords Choose Lockwell Finance

- Access to specialist BTL lenders

- Support for complex leasehold cases

- Guidance on short lease properties

- Limited company mortgage expertise

- Fast application support

- Experienced property finance advisers

Request a free consultation today and explore your leasehold investment options with confidence.

Frequently Asked Questions

Can you get a leasehold BTL mortgage with a short lease?

Yes, some lenders offer mortgages for short lease properties, but options become more limited below 80 years remaining.

What is the minimum lease length for a buy-to-let mortgage?

Most lenders require at least 70–85 years remaining at completion, although criteria vary between lenders.

Are leasehold flats harder to mortgage than freehold houses?

Generally yes. Leasehold properties involve additional risks such as diminishing lease terms, service charges, and ground rent obligations.

Do service charges affect buy-to-let affordability?

Yes. Lenders often consider service charges when assessing rental coverage and affordability calculations.

Can you extend the lease after buying a rental property?

Yes. Leaseholders usually gain legal rights to extend after owning the property for two years, although informal extensions may also be possible.

Is a leasehold flat a good investment property?

It can be. Many leasehold flats generate strong rental demand in urban areas, particularly near transport links and universities.