Understanding SPV Mortgage Rates

SPV mortgages, or Special Purpose Vehicle mortgages, are specifically designed for property investors who wish to purchase real estate through a limited company. This structure provides a range of benefits, particularly in the realm of buy-to-let investments. By utilizing an SPV, investors can separate their personal finances from their property investments, which can lead to significant tax advantages and risk mitigation. For instance, rental income generated through an SPV is typically taxed at the corporate tax rate, which can be lower than personal income tax rates, especially for higher earners.

The importance of SPVs in property investment cannot be overstated. They allow investors to manage their portfolios more effectively, providing a clear boundary between personal and business assets. This separation can be particularly beneficial in the event of financial difficulties, as it limits personal liability. Furthermore, SPVs can facilitate easier access to financing options, as lenders often view them as lower-risk entities compared to individual borrowers.

In the UK, understanding SPV mortgage rates is crucial for any investor looking to maximize their returns. These rates can vary significantly based on factors such as the lender’s assessment of risk, the investor’s credit history, and prevailing market conditions. By comparing SPV mortgage rates with traditional personal mortgage rates, investors can make informed decisions that align with their financial goals.

Company BTL Interest Rates Explained

Company buy-to-let (BTL) interest rates refer to the rates applied to mortgages taken out by limited companies for the purpose of purchasing rental properties. These rates are distinct from personal mortgage rates, primarily due to the different risk profiles associated with individual borrowers versus corporate entities. Lenders often assess company BTL applications with a focus on the company’s financial health, including its creditworthiness and rental income projections.

One of the key differences between company BTL interest rates and personal rates is the way interest is calculated. Company BTL rates may offer more favorable terms, particularly for higher-value properties or larger portfolios. Additionally, because the income generated through an SPV is subject to corporation tax rather than personal income tax, many investors find that the overall tax implications are more advantageous when using a company structure.

Moreover, lenders may also offer different loan-to-value (LTV) ratios for company BTL mortgages compared to personal mortgages. For instance, while personal BTL mortgages might allow for an LTV of up to 75%, company BTL mortgages can sometimes reach 80% or more, depending on the lender’s criteria. This flexibility can be particularly appealing for investors looking to leverage their capital effectively.

SPV vs Personal Rates: Key Differences

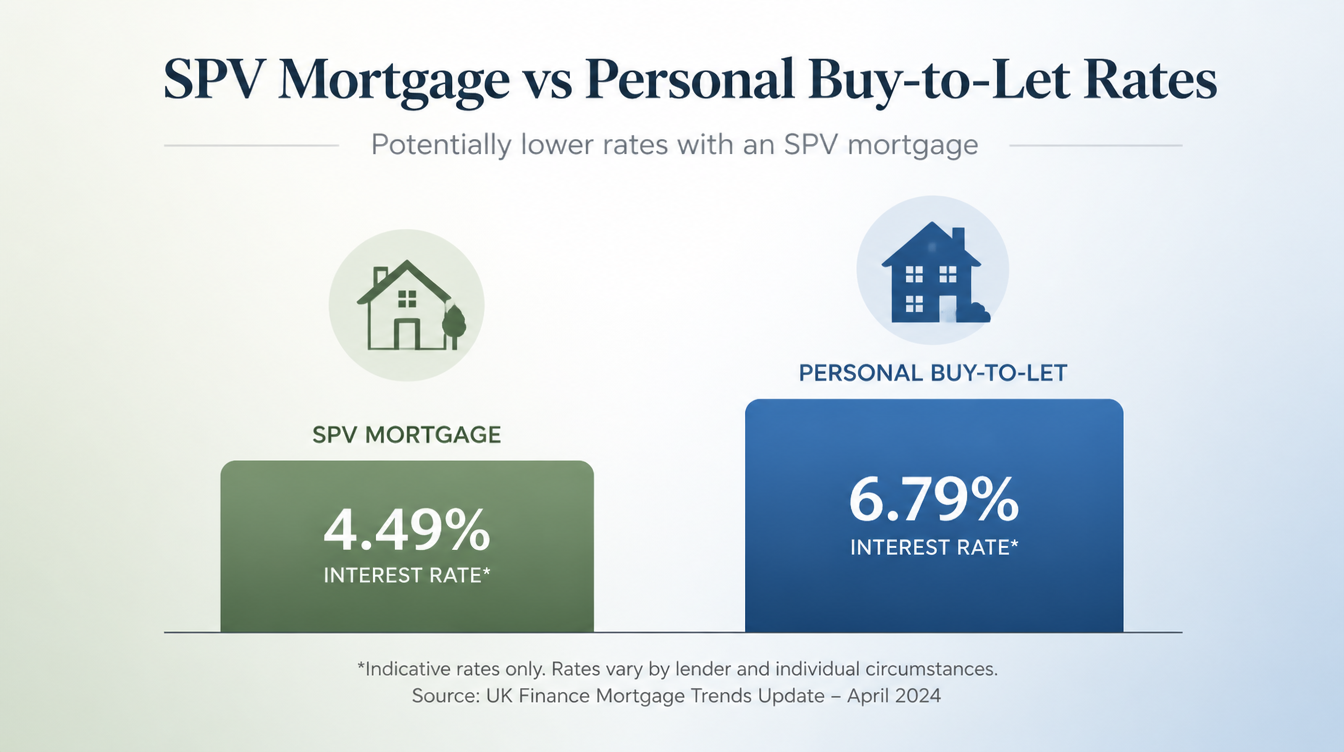

When comparing SPV mortgage rates with personal mortgage rates, several key differences emerge that can impact your investment strategy. Firstly, SPV mortgage rates often tend to be lower than personal rates. This is largely due to the perceived stability and reduced risk associated with lending to a limited company as opposed to an individual borrower. Lenders may view SPVs as more reliable, especially if the company has a solid financial history and a clear rental income strategy.

Another significant difference lies in the tax treatment of the income generated from the properties. Income from properties held in an SPV is subject to corporation tax, which is generally lower than personal income tax rates for higher earners. This tax efficiency can lead to substantial savings over time, making SPVs an attractive option for serious property investors.

Additionally, SPV mortgages can provide greater flexibility in terms of financing options. Investors may find that lenders are more willing to offer higher LTV ratios and more competitive terms for SPV mortgages. This can enable you to acquire properties with less upfront capital, allowing for a more aggressive investment strategy.

Ultimately, the decision between SPV and personal mortgage rates should be guided by your individual investment goals, financial situation, and the specific properties you intend to acquire. Consulting with a mortgage broker who specializes in buy-to-let investments can provide valuable insights tailored to your unique circumstances.

Factors Influencing SPV Mortgage Rates in the UK

Several factors can influence SPV mortgage rates in the UK, making it essential for investors to stay informed about market trends and lender criteria. One of the primary factors is the overall economic climate. Interest rates set by the Bank of England play a crucial role in determining mortgage rates. When the Bank of England raises interest rates to combat inflation, mortgage rates typically follow suit, affecting the cost of borrowing for SPVs.

Lender criteria also significantly impact SPV mortgage rates. Each lender has its own risk assessment process, which evaluates the financial health of the SPV, the credit history of the directors, and the projected rental income from the properties. A strong financial position and a solid rental income strategy can lead to more favorable mortgage rates.

Another important consideration is the type of property being financed. Lenders may have different risk appetites for various property types, such as residential, commercial, or mixed-use properties. For example, a lender may offer lower rates for residential properties due to their perceived stability compared to commercial properties, which may carry higher risks.

Finally, the investor’s experience and portfolio size can also influence SPV mortgage rates. Lenders often favor experienced investors with a track record of successful property management, which can lead to more competitive rates. Additionally, investors with larger portfolios may have more negotiating power when it comes to securing favorable terms.

Limited Company BTL Pricing in the UK

Limited company BTL pricing in the UK varies widely based on several factors, including lender policies, market conditions, and the investor’s financial profile. Generally, limited company BTL mortgages tend to have slightly higher rates than personal BTL mortgages due to the additional complexities involved in lending to a corporate entity. However, the tax benefits associated with using an SPV often outweigh the higher interest costs.

To find competitive rates, investors should conduct thorough research and consider working with a mortgage broker who specializes in limited company BTL mortgages. A broker can help you navigate the market, identify the best lenders, and negotiate favorable terms based on your unique circumstances.

Additionally, comparing rates across multiple lenders is crucial. Some lenders may offer promotional rates or discounts for specific property types or for first-time investors. Utilizing online mortgage comparison tools can also streamline this process, allowing you to quickly assess your options and make informed decisions.

It’s also worth noting that the fees associated with limited company BTL mortgages can vary. Some lenders may charge arrangement fees, valuation fees, or other costs that can impact the overall pricing. Understanding these fees upfront can help you accurately assess the total cost of borrowing and avoid any surprises down the line.

How to Secure the Best SPV Mortgage Rates

To secure the best SPV mortgage rates, there are several strategies you can employ to improve your chances of obtaining favorable terms. Firstly, maintaining a strong credit profile is essential. Lenders will assess your credit history and score when determining your eligibility and the rates they offer. Ensuring that your credit report is accurate and addressing any outstanding debts can significantly enhance your position.

Another effective strategy is to demonstrate a solid business plan for your property investments. Lenders want to see that you have a clear strategy for generating rental income and managing your properties effectively. This can include providing detailed projections of rental income, expenses, and your overall investment strategy.

Working with a mortgage broker who specializes in SPV mortgages can also be invaluable. A broker can provide insights into the best lenders for your specific situation and help you navigate the application process. They can also assist in presenting your case to lenders in the most favorable light, increasing your chances of securing competitive rates.

Finally, consider shopping around and comparing offers from multiple lenders. Different lenders may have varying criteria and rates, so taking the time to explore your options can pay off in the long run. By being proactive and informed, you can position yourself to secure the best SPV mortgage rates available in the market.

The Application Process for SPV Mortgages

The application process for SPV mortgages involves several key steps that investors should be aware of to ensure a smooth experience. First, you will need to gather the necessary documentation, which typically includes proof of identity, proof of income, and details regarding the properties you intend to purchase. Lenders will also require information about the SPV itself, including its registration and financial statements.

Once you have all the required documents, the next step is to submit your application to the lender. This can often be done online, making the process more convenient. During this stage, the lender will conduct a thorough assessment of your application, which may include a credit check and a review of the SPV’s financial health.

If the application is approved, the lender will issue a mortgage offer, outlining the terms and conditions of the loan. It is crucial to review this offer carefully, as it will detail the interest rate, repayment terms, and any associated fees. If you agree to the terms, you will need to sign the mortgage deed and complete any additional paperwork required by the lender.

Finally, the lender will arrange for a valuation of the property to ensure it meets their lending criteria. Once the valuation is complete and satisfactory, the funds will be released, allowing you to proceed with the purchase of the property. Throughout this process, staying in close communication with your mortgage broker can help address any questions or concerns that arise.

Frequently Asked Questions About SPV Mortgages

What are SPV mortgage rates?

SPV mortgage rates are specific rates for Special Purpose Vehicles used in property investment.

How do company BTL interest rates compare to personal rates?

Company BTL interest rates are often more favorable than personal rates due to tax benefits.

What factors affect SPV mortgage rates in the UK?

Market conditions, lender risk assessment, and borrower credit history.

Can I switch from a personal mortgage to an SPV mortgage?

Yes, but it involves a refinancing process and potential fees.

What documents do I need to apply for an SPV mortgage?

Proof of income, credit history, and details of the property investment.