If you are applying for a buy-to-let mortgage in the UK, one of the most important factors lenders assess is whether the expected rental income is high enough to cover the mortgage repayments. This is commonly referred to as rental coverage or the Interest Coverage Ratio (ICR).

Many landlords assume that a strong personal salary guarantees approval, but in reality, lenders focus heavily on the property’s projected rental income. Even experienced landlords can face rejection if the property does not meet the minimum rent requirements set by the lender.

Understanding the minimum rental income required for a BTL mortgage can help you choose the right property, avoid failed applications, and secure better mortgage terms.

Whether you are purchasing your first rental property or expanding a portfolio, this guide explains exactly how lenders calculate rental affordability, what ICR ratios mean, and how to improve your chances of approval.

Why Rental Income Matters for Buy-to-Let Mortgages

Unlike residential mortgages, buy-to-let mortgages are assessed primarily on the income the property is expected to generate.

Lenders want reassurance that:

- The monthly rent can comfortably cover mortgage repayments

- Landlords can manage interest rate increases

- The property remains profitable during void periods

- The investment remains sustainable over time

This is why lenders apply rental stress tests rather than relying solely on personal income.

In most cases, lenders use:

- Expected monthly rent

- Mortgage interest rate

- Interest Coverage Ratio (ICR)

- Tax status of the borrower

- Property type

- Portfolio size

What Is the Interest Coverage Ratio (ICR)?

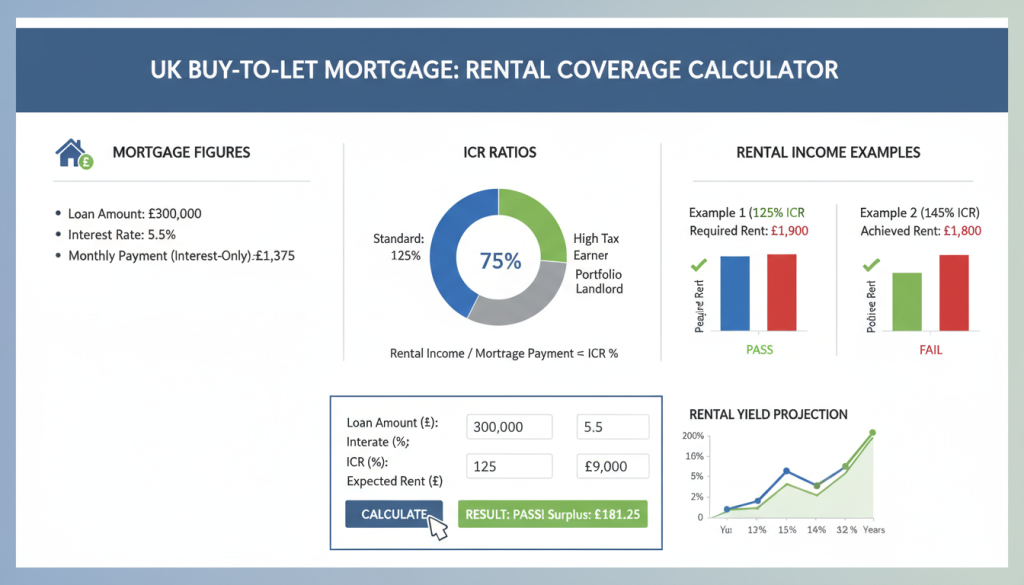

The Interest Coverage Ratio is the percentage of rental income required to cover the mortgage interest payments.

Most UK lenders require:

- 125% ICR for limited company landlords

- 145% ICR for higher-rate taxpayers

- Sometimes 130%–140% for basic-rate taxpayers

This means the rental income must exceed the mortgage payment by a set margin.

For example:

- Mortgage interest payment: £1,000 per month

- Required ICR: 145%

Minimum required rent:

- £1,000 × 145% = £1,450 monthly rent

This creates a financial buffer for lenders.

How Lenders Calculate Minimum Rental Income

Most lenders use a stress-tested interest rate instead of the actual product rate.

Typical stress rates range from:

- 5.0%

- 5.5%

- 6.0%

- Sometimes higher for portfolio landlords

The formula generally looks like this:

\text{Required Monthly Rent} = \frac{\text{Loan Amount} \times \text{Stress Rate}}{12} \times \text{ICR}

Example Calculation

Property purchase price: £300,000

Deposit: 25%

Loan amount: £225,000

Stress rate: 5.5%

ICR requirement: 145%

Step 1:

Annual stressed interest:

- £225,000 × 5.5% = £12,375

Step 2:

Monthly stressed interest:

- £12,375 ÷ 12 = £1,031.25

Step 3:

Apply 145% ICR:

- £1,031.25 × 145% = £1,495.31

Minimum required monthly rent:

- Approximately £1,500

Typical Minimum Rent Requirements by Property Value

| Property Value | Loan Amount (75% LTV) | Estimated Minimum Rent |

| £150,000 | £112,500 | £750–£850 |

| £250,000 | £187,500 | £1,200–£1,350 |

| £350,000 | £262,500 | £1,700–£1,950 |

| £500,000 | £375,000 | £2,400–£2,800 |

Actual figures vary depending on:

- Lender policy

- Tax status

- Product type

- Fixed-rate term

- Portfolio experience

Why Limited Company Landlords Often Need Lower Rental Coverage

Many lenders apply more favourable ICR calculations to limited company landlords because mortgage interest is treated differently for tax purposes.

Typical comparisons:

| Borrower Type | Common ICR |

| Individual higher-rate taxpayer | 145% |

| Limited company SPV | 125% |

| Basic-rate taxpayer | 125%–140% |

This can significantly improve borrowing capacity.

Example

An SPV landlord with a 125% ICR may qualify for:

- Larger loans

- Lower minimum rent requirements

- Improved affordability assessments

This is one reason why many portfolio landlords now purchase through limited companies.

Does Personal Income Matter?

Yes, but not always in the way landlords expect.

Some lenders require:

- Minimum personal income of £20,000–£30,000

- Evidence of employment or self-employed income

- Tax returns or payslips

However, some specialist lenders:

- Have no minimum income requirements

- Focus mainly on rental coverage

- Accept first-time landlords

- Accept foreign nationals and expatriates

Personal income becomes more important when:

- Rental coverage is tight

- The property is higher risk

- The landlord has limited experience

- The application involves adverse credit

What Happens if the Rental Income Is Too Low?

If the projected rent does not meet the lender’s minimum threshold, several things can happen:

Reduced Loan Amount

The lender may reduce the maximum borrowing amount.

Larger Deposit Required

You may need to increase your deposit to reduce the loan size.

Mortgage Declined

Some lenders will reject the application outright.

Higher Rates or Specialist Products

You may only qualify for specialist products with:

- Higher interest rates

- Additional fees

- Stricter underwriting

How Surveyors Assess Rental Income

Lenders usually instruct a surveyor to estimate the achievable market rent.

The surveyor considers:

- Local rental demand

- Comparable rental properties

- Property condition

- Property size

- EPC rating

- HMO licensing

- Tenant demand in the area

Even if you expect a certain rent, the lender uses the surveyor’s assessment — not the landlord’s estimate.

Minimum Rental Income for Different Property Types

Standard Single-Let Properties

These are the easiest properties to finance and usually have standard ICR requirements.

HMOs

HMO properties may generate stronger rental yields, but lenders often:

- Apply specialist criteria

- Require landlord experience

- Require licensing

- Use different stress testing

Student Lets

Student accommodation can provide strong yields but may involve:

- Seasonal void risks

- Specialist underwriting

- Portfolio analysis

Holiday Lets

Holiday lets are assessed differently and often require:

- Projected occupancy calculations

- Trading forecasts

- Specialist lenders

How to Improve Rental Coverage for a BTL Mortgage

Increase the Deposit

A larger deposit reduces the loan amount and lowers the required rent.

Choose Higher-Yield Areas

Properties with stronger yields improve affordability.

Purchase Through an SPV Limited Company

This can reduce the ICR requirement with some lenders.

Select a Longer Fixed Rate

Some lenders apply lower stress rates to:

- 5-year fixed products

- Longer-term products

This can increase borrowing capacity.

Improve the Property

Adding value through:

- Refurbishment

- Additional bedrooms

- Better EPC ratings

- Furnishing

can increase achievable rent.

Common Rental Stress Test Mistakes

Many landlords underestimate:

- Lender stress rates

- Surveyor rental assessments

- Tax impacts

- HMO licensing costs

- Void periods

A property that appears profitable on paper may fail affordability testing with multiple lenders.

Working with a specialist broker can help identify:

- Lenders with lower stress testing

- More flexible ICR calculations

- Portfolio-friendly lending criteria

- Limited company solutions

Real-World Example: Why Rental Coverage Matters

A landlord purchasing a flat in Manchester expected monthly rent of £1,400 and applied for a £250,000 BTL mortgage.

However:

- The surveyor assessed the rent at £1,250

- The lender required 145% ICR

- The application failed affordability

The landlord later:

- Increased the deposit

- Switched to a 5-year fixed product

- Applied through a limited company SPV

The revised application was approved.

This demonstrates how lender criteria can significantly affect borrowing power.

Key Factors That Influence Minimum Rent Requirements

Lenders consider:

- Loan-to-value ratio (LTV)

- Interest rate environment

- Fixed vs variable rate products

- Tax status

- Property type

- Portfolio size

- Experience level

- EPC regulations

- Market rental demand

No two lenders assess rental affordability in exactly the same way.

Why Professional Mortgage Advice Matters

BTL mortgage criteria can vary dramatically between lenders.

Some lenders:

- Use lower stress rates

- Accept top slicing

- Accept retained profits

- Support first-time landlords

- Specialise in portfolio lending

- Offer expat or foreign national products

A specialist broker can compare lender affordability models and help structure the application correctly from the beginning.

If you are unsure how much rental income your property needs to generate, speaking with an experienced broker before making an offer can prevent costly delays and rejected applications.

Frequently Asked Questions

What is the minimum rental income for a buy-to-let mortgage in the UK?

Most lenders require rental income to cover between 125% and 145% of the mortgage interest payments using a stress-tested rate.

What does 145% rental coverage mean?

It means the expected rental income must be 145% of the lender’s calculated monthly mortgage interest payment.

Can I get a BTL mortgage with low rental yield?

Possibly, but lenders may:

- Reduce borrowing

- Require a larger deposit

- Offer specialist products

- Decline the application

Do all lenders use the same ICR ratio?

No. ICR requirements vary between lenders depending on:

- Tax status

- Property type

- Fixed-rate term

- Portfolio size

Is minimum personal income required for a BTL mortgage?

Some lenders require minimum earned income, while others focus mainly on rental coverage and property performance.

Are limited company landlords treated differently?

Yes. Many lenders apply lower ICR requirements to limited company SPVs, which can improve affordability.

Final Thoughts

Understanding the minimum rental income required for a BTL mortgage is essential before purchasing any investment property.

The property may look profitable at first glance, but lender stress testing can produce very different results.

Before committing to a purchase:

- Calculate expected rental coverage carefully

- Compare lender stress tests

- Review tax implications

- Assess achievable market rent

- Speak with a specialist broker

The right mortgage structure can dramatically improve affordability and long-term profitability.

If you are planning a buy-to-let purchase, Lockwell Finance can help you compare lender criteria, maximise borrowing potential, and secure the most suitable mortgage solution for your investment strategy.