Understanding Stamp Duty for Mixed-Use Properties

Mixed-use properties are defined as real estate that combines residential and commercial elements within the same structure or development. This can include buildings with retail spaces on the ground floor and residential apartments above, or properties that serve dual purposes such as a café with living quarters. Understanding the implications of stamp duty on these properties is crucial for buyers, as it can significantly affect the overall cost of the purchase.

Stamp duty, specifically Stamp Duty Land Tax (SDLT) in the UK, is a tax levied on property purchases, and mixed-use properties have unique considerations compared to purely residential or commercial properties. The importance of understanding these implications cannot be overstated, as miscalculations or misunderstandings can lead to unexpected financial burdens. For instance, the stamp duty rates for mixed-use properties can differ from those for residential and commercial properties, which can impact your budget and financing options.

Moreover, the classification of a property as mixed-use can influence eligibility for certain reliefs and exemptions, making it vital to grasp how these factors interplay. By comprehensively understanding stamp duty for mixed-use properties, you can make informed decisions that align with your financial goals and ensure compliance with tax obligations.

How Mixed-Use Property Stamp Duty Differs

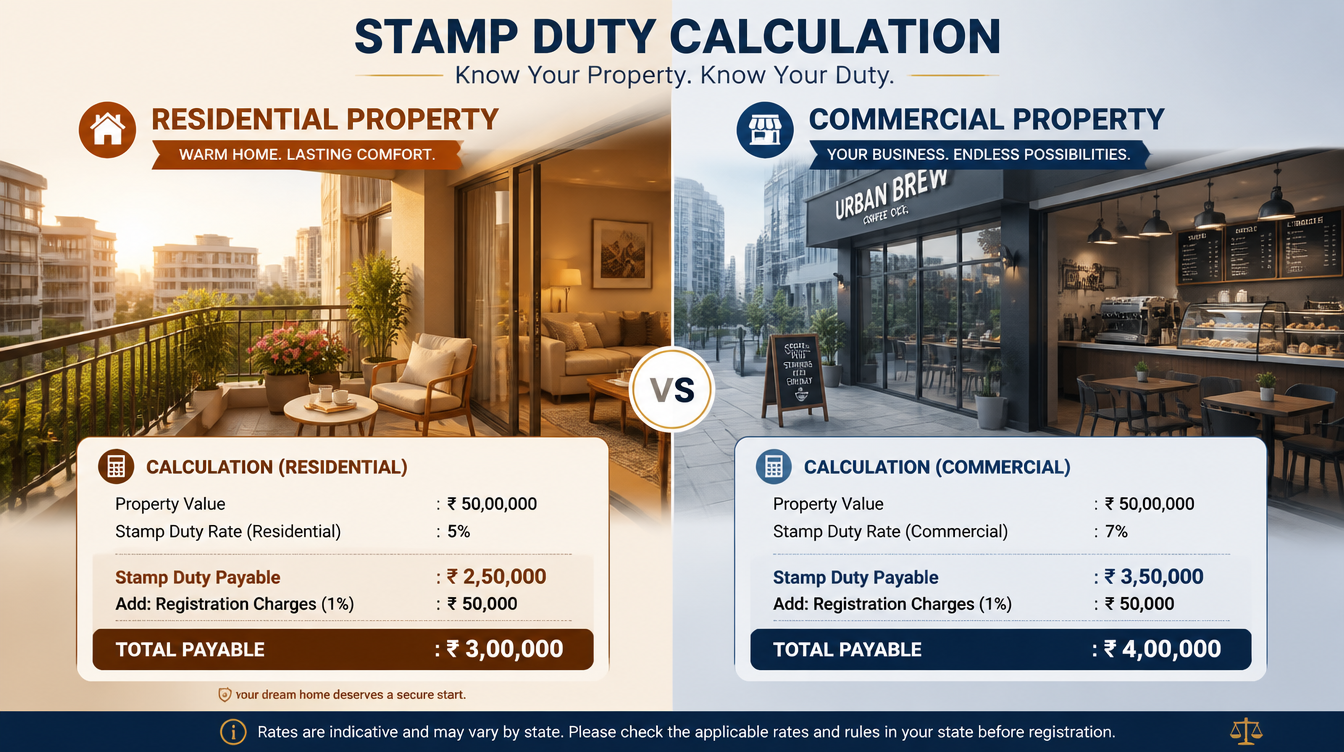

The stamp duty for mixed-use properties differs significantly from that for purely residential or commercial properties. For residential properties, the rates are generally lower and structured in a tiered system based on the purchase price. Conversely, commercial properties often incur higher rates due to their potential for generating income. Mixed-use properties, however, fall into a unique category that requires careful consideration of both residential and commercial rates.

One key factor influencing the stamp duty rate for mixed-use properties is the proportion of the property that is designated for commercial use versus residential use. If a property has a substantial commercial element, it may be subject to higher SDLT rates akin to commercial properties. For example, if a property is primarily used for retail purposes with only a small residential component, the stamp duty will lean towards commercial rates.

Additionally, the specific location of the property can also affect the stamp duty rate. Different regions in the UK may have varying rates and regulations concerning mixed-use properties. Therefore, understanding the local property market and regulations is essential to accurately assess the potential stamp duty liability.

In summary, the key differences in stamp duty for mixed-use properties arise from their hybrid nature, which requires a nuanced understanding of both residential and commercial tax implications. Buyers must consider the property’s usage, location, and the current SDLT rates to accurately calculate their potential tax liabilities.

Semi-Commercial SDLT: What You Need to Know

Semi-commercial properties are a specific subset of mixed-use properties that typically include a combination of residential and commercial elements, such as a shop with a flat above it. Understanding the SDLT applicable to semi-commercial properties is essential for potential buyers, as it can differ significantly from standard residential or commercial rates.

The SDLT rates for semi-commercial properties are structured to reflect the mixed-use nature of these properties. Generally, the rates are set at a lower threshold than those for purely commercial properties but higher than residential rates. For instance, while residential properties may have a starting rate of 0% for properties under £125,000, semi-commercial properties may start at a slightly higher threshold, reflecting their commercial potential.

As of now, the SDLT for semi-commercial properties is tiered based on the purchase price, similar to residential properties, but with specific rates that apply to the commercial portion. For example:

- 0% on the first £150,000 of the purchase price

- 2% on the portion between £150,001 and £250,000

- 5% on the portion above £250,000

These rates can vary based on the specific use of the property and any applicable reliefs or exemptions. It’s crucial to consult with a tax advisor or a property expert to ensure that you are aware of all potential costs and benefits associated with purchasing a semi-commercial property.

In conclusion, understanding the SDLT implications for semi-commercial properties is vital for making informed purchasing decisions. By being aware of the specific rates and regulations, you can better prepare for the financial responsibilities associated with your investment.

Calculating Stamp Duty for Mixed-Use Properties

Calculating stamp duty for mixed-use properties can be complex due to the varying rates applicable to residential and commercial components. Here’s a step-by-step guide to help you accurately calculate your stamp duty liability:

- Determine the Property Value: Start by establishing the total purchase price of the mixed-use property. This figure is critical as it will dictate the stamp duty rate applicable.

- Identify the Proportion of Commercial vs. Residential Use: Assess the property’s usage. If the property is 70% commercial and 30% residential, you’ll need to apply the commercial SDLT rates to the commercial portion and residential rates to the residential portion.

- Apply the Relevant SDLT Rates: Use the current SDLT rates for both the residential and commercial portions. For example, if the residential portion is valued at £200,000, you would apply residential rates to that value. If the commercial portion is valued at £300,000, apply the commercial rates to that portion.

- Calculate Each Portion: For the residential portion, if it falls under the residential SDLT thresholds, you may not owe any tax. For the commercial portion, calculate the tax owed based on the applicable rates.

- Combine the Totals: Finally, add the stamp duty amounts from both the residential and commercial calculations to arrive at your total stamp duty liability.

Common pitfalls in calculations include:

- Misjudging the Property Value: Ensure that you have an accurate valuation of the property to avoid underpayment or overpayment of stamp duty.

- Ignoring Local Regulations: Different regions may have specific rules regarding mixed-use properties, so it’s essential to stay informed about local regulations.

- Failing to Account for Reliefs: Some buyers may qualify for reliefs or exemptions that can significantly reduce their stamp duty liability. Always check for available options.

By following these steps and being mindful of common pitfalls, you can ensure a more accurate calculation of stamp duty for your mixed-use property purchase. If you have any uncertainties, consulting with a professional can provide clarity and peace of mind.

Commercial SDLT Rates in the UK

The current commercial SDLT rates in the UK are structured to reflect the potential income-generating capabilities of commercial properties. Understanding these rates is essential for buyers of mixed-use properties, as they may apply to the commercial portion of the property. The rates are tiered based on the purchase price, and they are as follows:

- 0% on the first £150,000

- 2% on the portion between £150,001 and £250,000

- 5% on the portion between £250,001 and £1,000,000

- 6% on the portion above £1,000,000

These rates apply to the commercial component of mixed-use properties. For instance, if you purchase a mixed-use property where the commercial portion is valued at £300,000, you would calculate the SDLT as follows:

- 0% on the first £150,000 = £0

- 2% on the next £100,000 (£150,001 to £250,000) = £2,000

- 5% on the remaining £50,000 (£250,001 to £300,000) = £2,500

In total, the SDLT owed on the commercial portion would be £4,500. It’s important to note that these rates can change, so always consult the latest government guidelines or a tax professional for the most accurate information.

In summary, understanding the commercial SDLT rates in the UK is crucial for anyone considering the purchase of a mixed-use property. By accurately calculating the potential tax liabilities, you can better plan your investment and ensure compliance with tax obligations.

Benefits of Understanding Your Stamp Duty Obligations

Understanding your stamp duty obligations when purchasing a mixed-use property offers several financial planning advantages. Firstly, it allows you to budget more accurately for your property purchase. By knowing the exact amount of stamp duty you will owe, you can ensure that you have sufficient funds available, avoiding any last-minute financial surprises.

Additionally, being aware of your stamp duty obligations helps you to avoid unexpected costs. Miscalculating your stamp duty can lead to penalties or additional fees, which can strain your finances. By understanding the rates and regulations, you can ensure that you are fully compliant and avoid any potential legal issues.

Moreover, understanding stamp duty can also open doors to potential reliefs or exemptions that may apply to your purchase. For example, certain first-time buyers may qualify for relief on stamp duty, significantly reducing their financial burden. By being informed, you can take advantage of these opportunities, making your investment more financially viable.

In conclusion, grasping your stamp duty obligations is not just about compliance; it’s a critical component of effective financial planning. By understanding the implications of stamp duty, you can make more informed decisions, budget accurately, and potentially save money on your property purchase.

How Lockwell Finance Can Assist You

At Lockwell Finance, we specialize in providing expert guidance and support for buyers navigating the complexities of mixed-use property purchases. Our team of experienced professionals can help you understand the intricacies of stamp duty and ensure that you are fully informed throughout the buying process.

We offer a range of services tailored to meet your specific needs, including:

- Personalized Consultation: Our experts will work with you to assess your unique situation and provide tailored advice on stamp duty implications.

- Accurate Calculations: We can assist you in accurately calculating your stamp duty liability, ensuring that you are fully aware of your financial obligations.

- Access to Reliefs: Our team will help you identify any potential reliefs or exemptions that may apply to your purchase, maximizing your savings.

- Ongoing Support: From initial consultation to final purchase, we provide continuous support to ensure a smooth transaction.

Don’t just take our word for it; here’s what some of our clients have to say:

“Lockwell Finance made the process of buying my mixed-use property so much easier. Their expertise in stamp duty saved me a significant amount of money.” – Sarah T.

“I was overwhelmed by the complexities of stamp duty, but the team at Lockwell Finance guided me through every step. Highly recommend!” – James R.

Contact us today to learn how we can assist you with your mixed-use property purchase and ensure that you understand all your stamp duty obligations.

Frequently Asked Questions

What is stamp duty for mixed-use properties?

Stamp duty is a tax on property purchases, including mixed-use properties. It is calculated based on the purchase price and varies depending on the proportion of residential and commercial use.

How is stamp duty calculated for mixed-use properties?

It involves assessing the property value and applying the relevant SDLT rates based on the residential and commercial components of the property.

What are the current commercial SDLT rates in the UK?

Rates vary based on property value and type; consult the latest government guidelines for the most accurate information.

Can I claim relief on stamp duty for mixed-use properties?

Certain reliefs may apply; it’s best to consult with a tax advisor to explore your options.

How can Lockwell Finance help with stamp duty calculations?

We provide expert advice and support to ensure accurate calculations and compliance with all stamp duty obligations.