Understanding the Overseas Mortgage Application Process

Securing an overseas mortgage can be a complex yet rewarding endeavor for those looking to invest in property outside their home country. An overseas mortgage allows individuals to finance the purchase of property in another country, often providing opportunities for investment, vacation homes, or relocation. However, the process differs significantly for non-residents compared to domestic buyers, particularly in the UK. Understanding these differences is crucial for a smooth application process.

One of the primary distinctions for non-residents is the requirement for documentation. Lenders typically demand a more extensive range of financial information, including proof of income, credit history, and identification. Non-residents may also face stricter lending criteria, as lenders assess the risk associated with lending to individuals who do not reside in the country where the property is located.

Furthermore, the types of mortgages available can differ. Non-residents might be limited to specific mortgage products, such as interest-only mortgages or those with higher deposit requirements. For instance, while a UK resident may secure a mortgage with a 10% deposit, non-residents may need to provide a deposit of 25% or more, depending on the lender’s policies.

Additionally, the interest rates offered to non-residents can be higher than those available to residents, reflecting the increased risk perceived by lenders. It’s also important to note that some lenders may charge additional fees for processing overseas applications, which can add to the overall cost of borrowing.

In summary, while overseas mortgages present exciting opportunities, non-residents must navigate a more intricate application process. Understanding the key differences and preparing accordingly can significantly enhance the chances of a successful application.

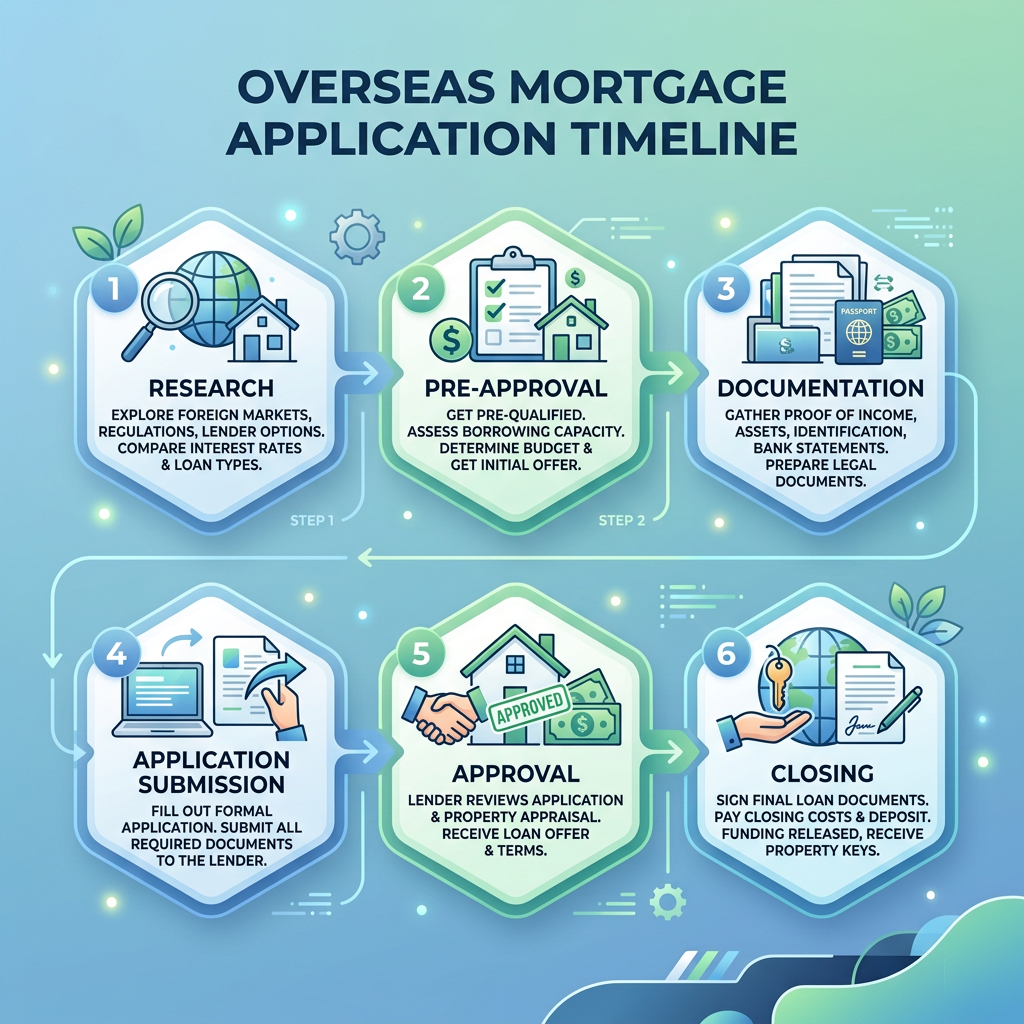

Step-by-Step Overseas Mortgage Timeline

The overseas mortgage application process can be broken down into several key stages, each with its own timeline and requirements. Here’s a detailed overview of what to expect:

- Initial Consultation and Documentation

The first step involves an initial consultation with a mortgage advisor or lender. During this meeting, you will discuss your financial situation, property goals, and the type of mortgage you are seeking. It’s essential to gather all necessary documentation, including:

- Proof of income (e.g., payslips, tax returns)

- Credit history reports

- Identification documents (passport, utility bills)

This stage typically takes 1-2 weeks, depending on how quickly you can gather the required documents.

- Pre-Approval Process

Once you have submitted your documentation, the lender will conduct a preliminary assessment of your financial situation to determine your eligibility for a mortgage. This pre-approval process usually takes 1-3 weeks. It’s advisable to obtain pre-approval before making any offers on properties, as it gives you a clearer idea of your budget and strengthens your position as a buyer.

- Formal Application Submission

After securing pre-approval, you will need to submit a formal mortgage application. This includes providing additional documentation and details about the property you intend to purchase. The lender will also require a valuation of the property, which can take an additional 1-2 weeks. The formal application stage can take 2-4 weeks, depending on the lender’s processing times.

- Underwriting and Approval

During the underwriting phase, the lender will thoroughly assess your application, including your financial stability and the property’s value. This stage can take anywhere from 2 to 6 weeks, depending on the complexity of your application and any additional information the lender may require. Once approved, you will receive a formal mortgage offer detailing the terms and conditions of your loan.

- Completion and Funding

The final step is the completion of the mortgage process, where legal documents are signed, and funds are transferred. This stage can vary in duration, typically taking 1-3 weeks, depending on the efficiency of the solicitors involved and any legal checks that need to be completed. Once completed, you will officially own the property.

In total, the overseas mortgage application timeline can range from approximately 6 to 12 weeks, depending on various factors such as lender processing times and the complexity of your application.

Factors Affecting the Overseas Mortgage Timeline

Several factors can influence the timeline of an overseas mortgage application. Understanding these can help you anticipate potential delays and prepare accordingly.

- Type of Property and Location

The type of property you are purchasing and its location can significantly impact the mortgage timeline. Properties in popular areas may require quicker valuations due to higher demand, while unique or rural properties may take longer to assess.

- Financial Documentation Requirements

Non-residents often face more stringent documentation requirements. Gathering the necessary paperwork can be time-consuming, especially if you need to obtain documents from overseas. Delays in providing these documents can extend the application timeline.

- Lender Processing Times

Each lender has different processing times based on their internal systems and workload. Some lenders may offer faster processing for overseas applications, while others may take longer due to additional checks and assessments required for non-residents.

- Legal Considerations for Non-Residents

Legal requirements can vary significantly for non-residents, potentially adding to the timeline. Engaging a local solicitor familiar with overseas transactions can help streamline this process, but it’s essential to factor in the time needed for legal checks and compliance.

Common Delays in the Overseas Mortgage Process

While the overseas mortgage process is generally straightforward, several common delays can arise. Being aware of these can help you mitigate potential issues:

- Issues with Documentation

Missing or incomplete documentation is one of the most common causes of delays. Ensure that all paperwork is accurate and submitted promptly to avoid setbacks. Double-check that you have all required documents before submitting your application.

- Valuation Delays

Valuation delays can occur if the property is in a less accessible location or if the valuation firm is busy. Scheduling the valuation early in the process can help minimize this risk.

- Legal Complications

Legal issues, such as disputes over property titles or zoning regulations, can lead to significant delays. Engaging a knowledgeable solicitor can help navigate these complexities and expedite the process.

- Communication Gaps with Lenders

Communication gaps between you, your solicitor, and the lender can lead to misunderstandings and delays. Regularly check in with all parties involved to ensure everyone is on the same page and that any issues are addressed promptly.

Tips for a Smooth Overseas Mortgage Application

To enhance your chances of a successful and timely overseas mortgage application, consider the following tips:

- Preparing Documentation in Advance

Gather all necessary documentation before starting the application process. This includes proof of income, credit history, and identification. Having everything ready can significantly speed up the initial stages of your application.

- Choosing the Right Lender

Research lenders that specialize in overseas mortgages for non-residents. Some lenders may offer more favorable terms or faster processing times for international buyers. Compare different options to find the best fit for your needs.

- Understanding Local Regulations

Familiarize yourself with the local regulations regarding property purchases as a non-resident. This knowledge can help you avoid potential legal pitfalls and streamline the application process.

- Engaging a Local Solicitor

Hiring a local solicitor with experience in overseas transactions can be invaluable. They can assist with legal checks, ensure compliance with local laws, and help navigate any complexities that arise during the process.

Real-Life Case Studies of Overseas Buyers

To illustrate the overseas mortgage process, let’s explore some real-life case studies that highlight both successful applications and challenges faced by overseas buyers.

Case Study 1: Successful Purchase in Spain

A British couple sought to purchase a vacation home in Spain. They engaged a mortgage broker specializing in overseas mortgages, who guided them through the application process. By preparing their documentation in advance and securing pre-approval, they managed to complete their purchase within eight weeks. Their proactive approach and the broker’s expertise were key factors in their success.

Case Study 2: Challenges in France

Another buyer faced significant delays when purchasing a property in France. The buyer underestimated the time needed to gather financial documentation and encountered valuation delays due to the property’s unique features. By the time they resolved these issues, their application took over 12 weeks. This experience highlighted the importance of thorough preparation and understanding local processes.

Case Study 3: Overcoming Legal Complications in Italy

A buyer looking to invest in Italy faced legal complications related to zoning regulations. They initially engaged a solicitor unfamiliar with local laws, which led to misunderstandings and delays. After switching to a local expert, they were able to navigate the legal landscape effectively, ultimately completing their purchase in just under ten weeks. This case underscores the importance of choosing the right legal representation.

These case studies demonstrate that while the overseas mortgage process can present challenges, with the right preparation and support, buyers can successfully navigate the complexities and achieve their property goals.

Frequently Asked Questions About Overseas Mortgages

What is the average timeline for an overseas mortgage?

Typically ranges from 6 to 12 weeks depending on various factors.

Can I get an overseas mortgage as a non-resident?

Yes, many lenders offer options for non-residents.

What documentation do I need for an overseas mortgage?

Proof of income, credit history, and identification are essential.

Are there additional costs involved in overseas mortgages?

Yes, costs may include legal fees, valuation fees, and stamp duty.

How can I expedite the overseas mortgage process?

Prepare all documentation in advance and choose a responsive lender.