Understanding Bridging Loans

Bridging loans are short-term financing solutions designed to provide immediate funds for property transactions. They are typically used to bridge the gap between the purchase of a new property and the sale of an existing one, making them a vital tool in the real estate market. These loans are particularly beneficial when quick access to capital is necessary, such as in competitive property markets or urgent financial situations.

Common uses for bridging loans include:

- Property Purchases: Buyers often utilize bridging loans to secure a new property before selling their current home, ensuring they do not miss out on a desirable purchase.

- Renovation Projects: Investors may use bridging finance to fund refurbishment projects, allowing them to enhance property value before refinancing or selling.

- Auction Purchases: Bridging loans are frequently employed by buyers at property auctions, where quick payment is required to secure a deal.

- Probate Situations: Executors of estates may need bridging finance to manage property sales while awaiting the resolution of estate matters.

Bridging loans can be secured against residential or commercial properties and are typically more flexible than traditional mortgages. However, they often come with higher interest rates due to the short-term nature and perceived risk. Understanding the various interest structures available, such as rolled up and monthly interest, is crucial for borrowers to make informed financial decisions.

What is Rolled Up Interest?

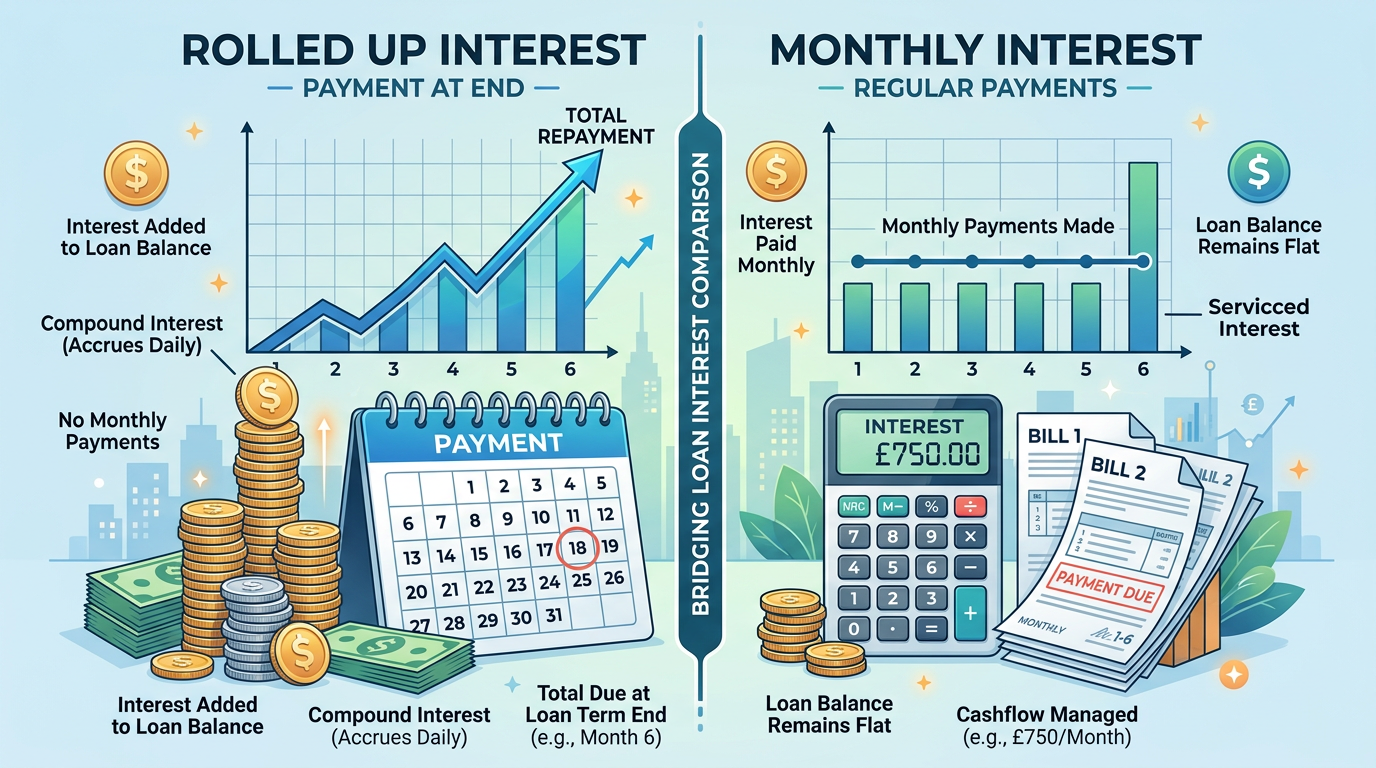

Rolled up interest refers to a method of charging interest on a loan where the interest payments are added to the principal amount rather than being paid out monthly. This means that borrowers do not have to make regular interest payments during the loan term; instead, the total interest accrued is repaid at the end of the loan period along with the principal.

In practice, rolled up interest can be particularly advantageous for those who may not have sufficient cash flow to cover monthly payments. For instance, if a borrower takes out a bridging loan of £100,000 with a rolled up interest rate of 10% over a 12-month period, the total interest accrued would amount to £10,000. At the end of the term, the borrower would repay £110,000.

This structure allows borrowers to focus on their immediate financial needs without the burden of monthly payments. However, it is essential to understand that while rolled up interest can ease cash flow constraints, it can also lead to a significantly larger total repayment amount at the end of the loan term, which can be a critical factor in decision-making.

What is Monthly Interest?

Monthly interest refers to a payment structure where borrowers make regular interest payments on their loan every month. This approach allows borrowers to manage their cash flow more effectively, as they are not accumulating additional interest on the principal amount throughout the loan term.

With monthly interest, borrowers can expect to pay a fixed amount each month based on the interest rate and the outstanding loan balance. For example, if a borrower takes out a £100,000 bridging loan at a 10% annual interest rate, the monthly interest payment would be approximately £833.33. Over a 12-month period, the total interest paid would amount to £10,000, but the principal remains unchanged until the end of the loan term.

The advantages of monthly interest payments include:

- Predictability: Borrowers can budget their monthly expenses more effectively with fixed payments.

- Lower Total Interest: By making monthly payments, borrowers can reduce the total interest paid over the life of the loan, as the principal balance decreases.

- Improved Cash Flow Management: Regular payments can help borrowers stay on top of their financial obligations and avoid a large repayment at the end of the term.

Choosing between rolled up and monthly interest depends on individual financial circumstances and preferences, making it essential to evaluate both options carefully.

Comparing Rolled Up vs Monthly Interest

When considering bridging loan options, understanding the key differences between rolled up and monthly interest is crucial. Here are the primary distinctions:

- Payment Structure: Rolled up interest accumulates and is paid at the end of the loan term, while monthly interest requires regular payments throughout the loan period.

- Cash Flow Impact: Rolled up interest can ease immediate cash flow constraints, making it suitable for borrowers who may not have enough liquidity. In contrast, monthly interest payments can help manage cash flow more predictably.

- Total Repayment Amount: Borrowers opting for rolled up interest may face a larger total repayment amount due to the accumulation of interest, whereas monthly interest may lead to lower overall costs.

- Flexibility: Rolled up interest may offer more flexibility for short-term financial needs, while monthly interest provides a structured repayment plan.

When deciding which option to choose, borrowers should consider their financial situation, the purpose of the loan, and their ability to make regular payments. For instance, if a borrower is confident in their cash flow and prefers to minimize overall costs, monthly interest may be the better choice. However, if immediate liquidity is a concern, rolled up interest could provide the necessary financial relief.

Retained Interest Bridging Explained

Retained interest is another type of interest structure in bridging loans, which differs from both rolled up and monthly interest. In this scenario, the lender retains a portion of the loan amount as interest, which is deducted from the total loan disbursement. For example, if a borrower applies for a £100,000 loan with a retained interest rate of 10%, the lender may disburse only £90,000 to the borrower, retaining £10,000 as interest.

This structure can be beneficial for borrowers who prefer to receive a lower initial amount while still having the flexibility of not making monthly payments. The retained interest is settled at the end of the loan term along with the principal. Essentially, the borrower receives less upfront but avoids the burden of monthly payments, similar to rolled up interest.

Key differences between retained interest and the other two structures include:

- Initial Loan Amount: Borrowers receive a reduced amount upfront, which can impact their purchasing power.

- Payment Timing: Like rolled up interest, retained interest is paid at the end of the loan term, allowing for immediate cash flow relief.

- Financial Planning: Borrowers must factor in the reduced initial loan amount when planning their finances, as it may affect their ability to complete property transactions.

Understanding retained interest bridging can help borrowers make informed decisions about their financing options, particularly in scenarios where cash flow is a primary concern.

Bridging Interest Types in the UK

In the UK, various bridging interest types are available, catering to different borrower needs and financial situations. The primary types include:

- Rolled Up Interest: As discussed, this type allows borrowers to add interest to the principal amount, repaying it at the end of the loan term.

- Monthly Interest: This structure involves regular monthly payments, providing predictability and potentially lower total repayment amounts.

- Retained Interest: This option involves the lender retaining a portion of the loan as interest, providing the borrower with a reduced upfront amount.

Regulations affecting bridging loans in the UK are primarily governed by the Financial Conduct Authority (FCA). Borrowers should be aware of the following regulations:

- Affordability Assessments: Lenders must conduct thorough assessments to ensure borrowers can afford the loan, taking into account their financial situation and repayment ability.

- Transparency Requirements: Lenders are required to provide clear information about loan terms, including interest rates and fees, ensuring borrowers understand their obligations.

- Consumer Protection: Regulations are in place to protect consumers from unfair lending practices, ensuring a fair and transparent borrowing process.

Understanding these regulations and interest types is essential for borrowers seeking bridging loans in the UK, as it can significantly impact their borrowing experience and financial outcomes.

Case Studies: Real-Life Scenarios

To illustrate the practical applications of rolled up and monthly interest, consider the following case studies:

Case Study 1: Rolled Up Interest

A property investor needed £200,000 to purchase a new investment property quickly. They opted for a bridging loan with a rolled up interest structure at a 12% annual rate over a 12-month term. Instead of making monthly payments, the investor allowed the interest to accumulate, resulting in a total repayment of £224,000 at the end of the term. This option provided the investor with immediate access to funds without impacting their cash flow during the renovation period.

Case Study 2: Monthly Interest

In a different scenario, a homeowner needed £150,000 to secure a new home while their current property was on the market. They chose a bridging loan with a monthly interest payment structure at an 8% annual rate. This resulted in monthly payments of approximately £1,000. By making regular payments, the homeowner managed their cash flow effectively and reduced the total interest paid over the loan term, ultimately repaying £156,000 at the end of the loan period.

These case studies highlight the importance of selecting the right interest structure based on individual financial needs and circumstances, demonstrating how each option can serve different borrower profiles effectively.

Choosing the Right Option for Your Needs

When selecting between rolled up and monthly interest options for bridging loans, several factors should be considered:

- Cash Flow: Evaluate your current cash flow situation. If you have limited liquidity, rolled up interest may provide the necessary flexibility.

- Financial Goals: Consider your long-term financial goals. If minimizing total interest payments is a priority, monthly interest may be the better choice.

- Loan Purpose: Assess the purpose of the loan. For quick property purchases or urgent financial needs, rolled up interest could be advantageous.

- Repayment Ability: Be realistic about your ability to make monthly payments. If you anticipate challenges in meeting regular obligations, rolled up interest may be more suitable.

Additionally, consulting with a financial advisor or bridging loan specialist can provide valuable insights tailored to your specific situation, helping you navigate the complexities of bridging finance effectively.

Conclusion

Understanding how interest is charged on bridging loans is essential for making informed financial decisions. Both rolled up and monthly interest structures offer unique advantages and drawbacks, catering to different borrower needs. By carefully evaluating your financial situation, loan purpose, and repayment capabilities, you can choose the option that best aligns with your goals.

Ultimately, bridging loans can provide a vital solution for property transactions, and selecting the right interest type is a critical step in ensuring a successful borrowing experience.

Frequently Asked Questions

What is the difference between rolled up and monthly interest on bridging loans?

Rolled up interest is added to the loan amount, while monthly interest is paid regularly.

When should I choose rolled up interest for my bridging loan?

Consider rolled up interest if you prefer not to make monthly payments or have cash flow constraints.

Are there any risks associated with rolled up interest?

Yes, it can lead to a larger total repayment amount at the end of the loan term.

Can I switch from rolled up to monthly interest during the loan term?

Typically, this is not allowed; consult your lender for specific terms.

What are the common fees associated with bridging loans?

Fees may include arrangement fees, valuation fees, and legal fees.